Update your browser to view this website correctly. Outdated Browser

For online banking click here.

|

Annual Disclosures |

Documents |

|---|---|

| For the year ended 31-12-2023 |

|

| For the year ended 31-12-2022 |

|

|

Quarterly Disclosures |

Documents |

|---|---|

| 2023 | |

| As at 30-09-2023 |

|

| As at 30-06-2023 |

|

| As at 31-03-2023 |

|

| 2022 | |

| As at 30-09-2022 |

|

| As at 30-06-2022 |

|

| As at 31-03-2022 |

|

| Annual Disclosures | Documents |

|---|---|

| Assessment Exercise - 2023 |

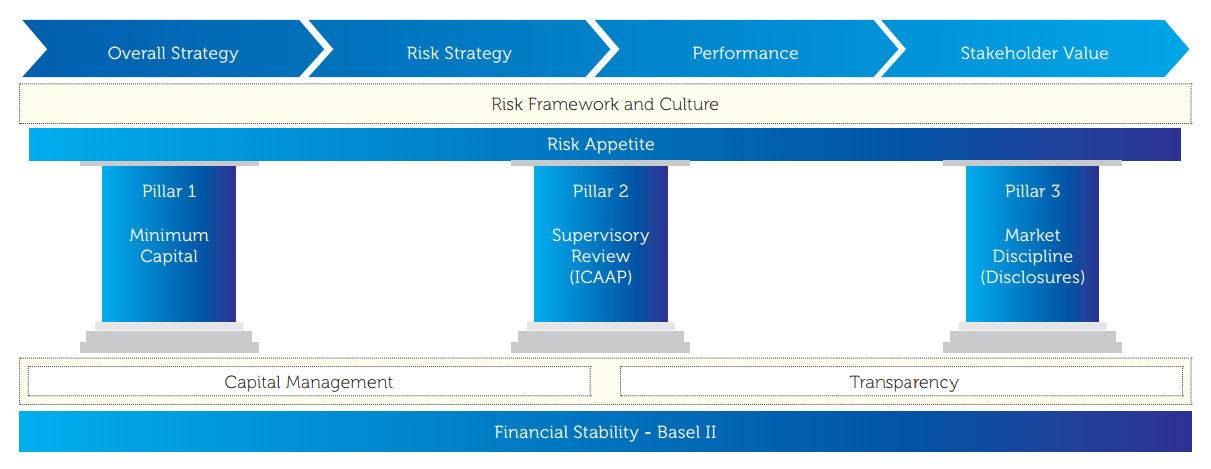

A clear understanding of risks surrounding the business activities is essential for any organisation to create sustainable stakeholder value through executing its strategies. It is therefore, essential to reinforce the overall strategy of an organisation with a prudent risk management strategy so that the opportunities could be optimised while minimising the effects of down-side risks. Banks which are responsible for the vital role of financial intermediation in the economy should be more committed to managing their risks in a prudent and transparent manner compared to a normal business organisation. Accordingly, Basel Committee on Banking Supervision has formulated broad supervisory standards and guidelines to inculcate industry best practices across the banking institutions through ‘Basel Accords’ (Basel II, the second of the Basel Accords which has been extended by Basel III). While Basel Accord encourages convergence towards common approaches and standards, the ultimate purpose of these rules is to create financial stability and resilience in financial sector institutions.

If you`d like more help & information, you can: