Commercial Bank’s risk and capital management framework is firmly anchored in the three pillars of the Basel regulatory framework. These principles are deeply embedded in our governance structure, decision-making processes, and risk oversight practices. They guide how the Bank identifies, measures, and manages risk while maintaining capital strength and operational resilience.

Pillar I: Capital Adequacy

The Bank calculates its capital adequacy in full compliance with the Banking Act Directions on Capital Requirements under Basel III, as issued by the Central Bank of Sri Lanka (CBSL).

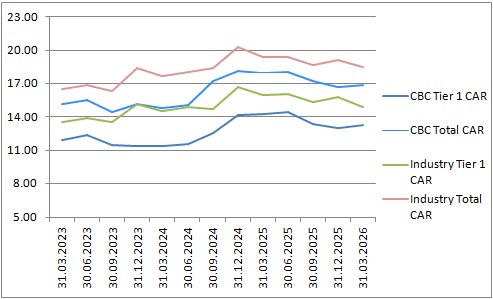

As of 31 December 2024, the Bank’s total Risk-Weighted Assets (RWA) stood at LKR 1.574 trillion, up from LKR 1.371 trillion at end-2023, an increase of approximately 14.86%. This rise in RWAs was driven primarily by increased lending activity across corporate, SME, and retail portfolios, reflecting stronger business volumes. In addition, changes in the composition of credit exposures and necessary re-classification under regulatory standards contributed to the higher risk weighting. The Country downgrade of Maldives led to higher risk weightings on exposures to Maldivian sovereigns and central banks, resulting in changes to related claims. In addition, risk–weighted assets for Market Risk increased, primarily due to heightened interest rate risk associated with Bangladesh Government Securities. Despite the increase in RWAs, the Bank strengthened its capital base. Tier 1 and Total Capital ratios improved to 14.227% and 18.142% respectively, well above the regulatory minimums of 10.00% and 14.00% respectively.

To ensure capital sustainability, the Bank raised fresh capital in 2024 via a rights issue, raising LKR 22.544 billion, which strengthened Tier 1 capital considerably. Combined with the year’s retained earnings and prudent dividend policy, this supports long-term capital resilience even as RWAs grow.

Under the Bank’s internal capital planning process, regular stress testing is conducted under the Internal Capital Adequacy Assessment Process (ICAAP). These stress tests, including severe but plausible macroeconomic scenarios, show that the Bank’s capital base remains well above regulatory minimums. This demonstrates the Bank’s ability to absorb unexpected shocks, while continuing to support business growth and a growing loan book.

Pillar II: Internal Assessment & Oversight (ICAAP)

The ICAAP process first implemented in 2013, has evolved into a comprehensive and forward-looking framework that assesses the adequacy of the Bank’s capital relative to its overall risk exposure.

This process goes beyond the minimum regulatory requirements of Pillar I by incorporating all material risks of credit concentration, interest rate risk in the banking book, liquidity, reputational, strategic, and emerging risks. It is subject to an annual independent review and Board approval, with oversight from the Executive Integrated Risk Management Committee (EIRMC).

The ICAAP employs advanced stress testing and scenario analysis to evaluate the potential impact of severe but plausible macroeconomic events on the Bank’s financial position,emanating from all plausible risks.

The ICAAP assessment determines the Pillar II capital requirements too, reflecting the Bank’s internal view of its aggregate risk tolerance and the capital needed to remain resilient under a wide range of conditions.

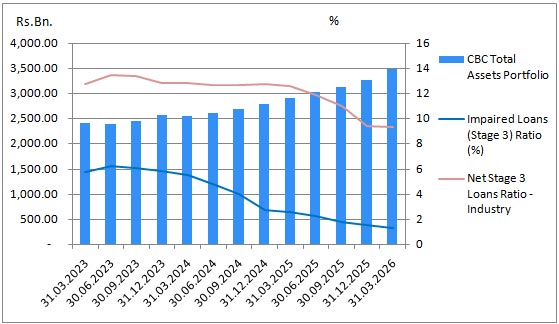

As of December 31, 2024, several key risk indicators remain safely within internal policy thresholds: the impaired-loans (Stage 3) ratio stands at 3.05% (policy range 2–5%); provision cover for Stage 3 loans is 64.61% (well above earlier years); concentration metrics such as sectoral exposure (HHI 0.0111), large-exposure aggregate (16.88% of eligible capital), and single-product exposure (35.01% of loan portfolio) remain comfortably within internal limits; the interest-rate repricing gap is 0.84 (below the internal maximum of 1.5); liquidity metrics are strong (LCR 454.36%, NSFR 187.29%).

Considering these metrics, the Bank’s internal capital planning confirms that there is sufficient buffer to absorb stress-scenarios while supporting ongoing business and balance sheet growth. Stress tests under ICAAP, which simulate severe economic downturns and combined risk events, show that capital remains above internal target thresholds.

These analyses demonstrate that even under severe macroeconomic stress, the Bank maintains capital above internal thresholds, confirming the strength and depth of its risk governance practices.